Where oil will be trading in January 2032

Why a lower price for oil means things could get worse for alternative energy companies before they get better

(Mark Hulbert, an author and longtime investment columnist, is the founder of the Hulbert Financial Digest; his Hulbert Ratings audits investment newsletter returns.)

CHAPEL HILL, N.C. (Callaway Climate Insights) — The price of oil is likely to remain low for a very long time. While that’s good news for efforts to reduce fossil fuel production and use, it ironically creates headaches for alternative energy companies.

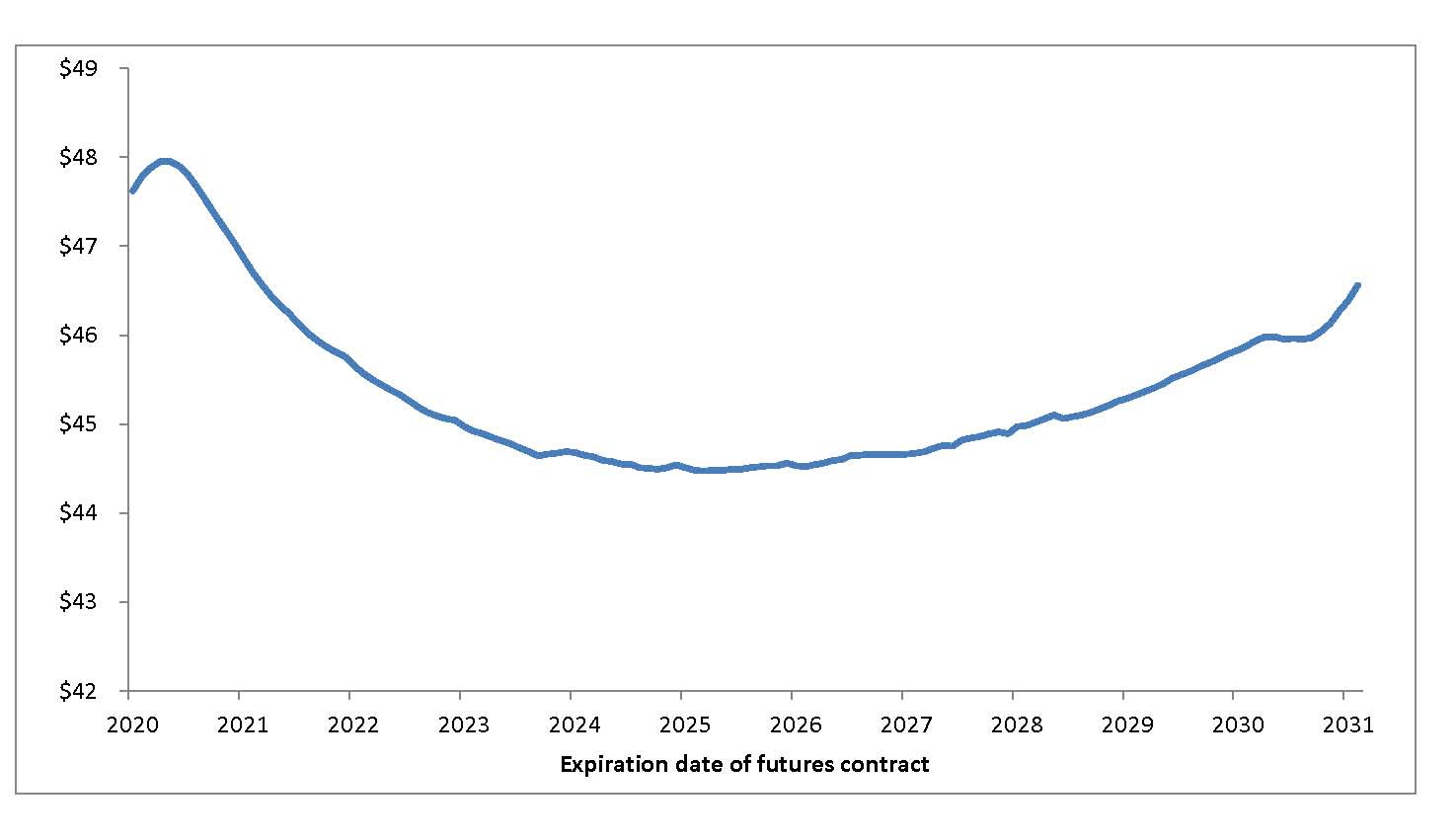

Take a look at the accompanying chart, which plots the “futures curve” for West Texas Intermediate crude oil — the prices at which the contracts of varying expirations are trading. Notice that the contracts that expire anywhere from nine months to a decade from now are trading for lower than oil’s spot price.

A bearish picture

The futures curve for West Texas Intermediate crude oil

Take the futures contract that extends the furthest into the future, expiring in January 2032. It currently trades for $46.56 per barrel, more than a dollar per barrel lower than the current spot price of $47.62. If we discount that 2032 price into today’s dollars using the 10-year breakeven inflation rate, we realize that futures traders collectively are betting that oil’s price in inflation-adjusted terms will be 20% lower than today in slightly more than 11 years’ time.

This has profound consequences for the petroleum industry, needless to say. Less obvious is that it will also greatly affect the market for alternative energy, much of which is competitive only if oil’s price is far higher. That suggests that, for alternative energy companies, things may become a lot worse before they get better.

For further insight into what the oil futures market may be telling us, I turned to K. Geert Rouwenhorst, professor of corporate finance at Yale University and deputy director of its International Center for Finance. In an interview, he said there’s nothing stopping futures traders who think the market is wrong from bidding the long end of the futures curve higher. That they’re not sends a strong signal.

Rouwenhorst added that the long end of the futures curve is different in this regard from the front end. That’s because futures contracts that expire relatively soon can be skewed by the cost of storage: A high cost of storage can inhibit speculators who otherwise would want to bet on higher prices, artificially depressing the prices of futures contracts that expire in a month or two. This is what we saw last spring, for example, when the spot oil contract briefly traded as low as minus $38 per barrel.

But, Rouwenhorst added, storage costs will not be artificially depressing the price of a futures contract expiring in 11 years.

Impact on the alternative energy market

In focusing on the headaches that a sustained period of low oil prices will have on the alternative energy market, I don’t want to minimize the good news that a low oil price contains for efforts to reduce fossil fuel use. Oil exploration and production that would have been profitable at higher prices becomes unprofitable at current low prices. New capital projects that were already in the pipeline, so to speak, get scrapped.

There’s a less-appreciated consequence of an extended period of low oil prices, Rouwenhorst added: If oil companies don’t foresee a return to profitability anytime soon, they may choose to flood the market with their oil in order to extract as much value as they can, while they can, from their proven reserves that are at risk of becoming stranded assets. This in turn could precipitate a downward spiral of lower and lower prices — a “race to the bottom,” as he put it.

Until that process has played itself out, alternative energy companies will be at a competitive disadvantage. In order to not just survive but to grow to the point they can be major suppliers of energy, they most likely will need legislative and regulatory support. This could take any of a number of forms, from direct subsidies to alternative energy companies to a carbon tax that makes oil’s effective price higher than it would be otherwise.

It no doubt seems paradoxical that the alternative energy industry would require this government support at the very time it seems as though the oil industry is itself on the ropes. But it’s precisely because the oil producers are suffering and have reduced chances of returning anytime soon to their previous levels of profitability that alternative energy companies are especially vulnerable.

As is often the case, the stock market in a collective sense appears to recognize this industry’s need for governmental support — even if many individual investors seem unaware of how precarious the industry is because oil is likely to stay low for many years. President-elect Joe Biden is considered far more supportive of the alternative energy industry than President Donald Trump has been, and stocks in that industry have soared as Biden’s victory has become more established.

Over the past month, as judged by a basket of the 10 largest clean-energy ETFs, alternative energy stocks have risen 9.0%, versus just 1.8% for the S&P 500 itself.